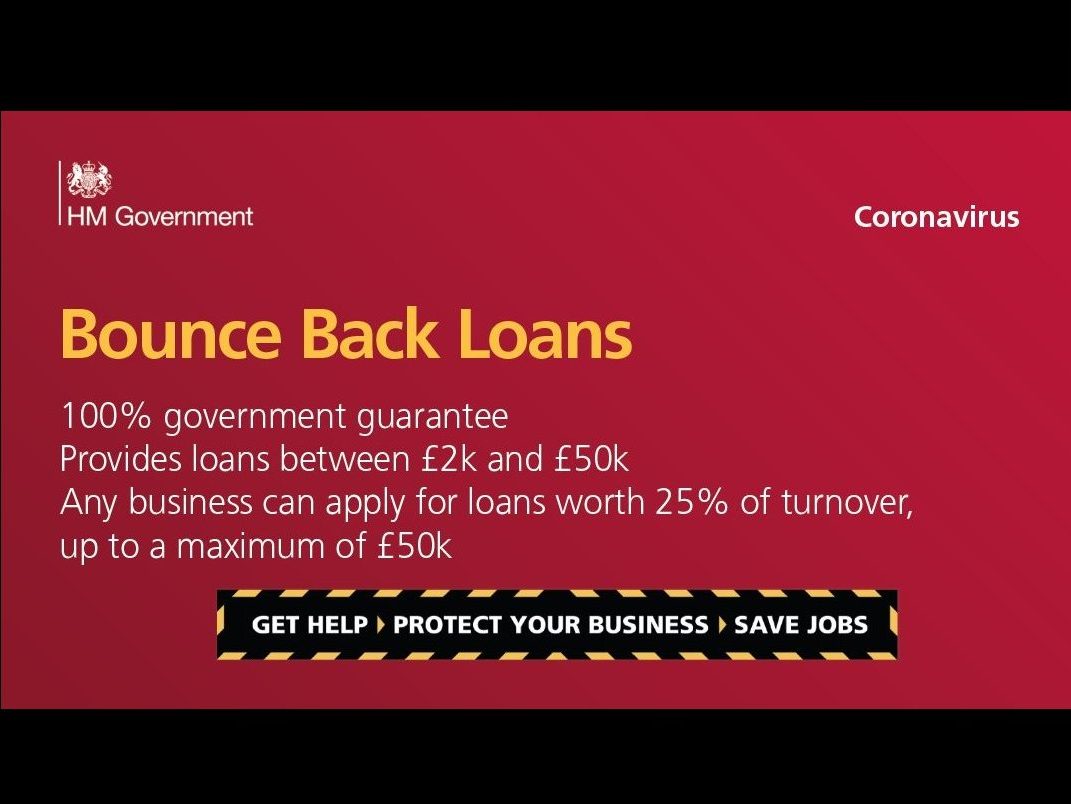

Hi folks The big announcement this week was Sunak's introduction of the so-called 'Bounce Back' loan schemes. We've also had a few self-employed clients asking about whether they can get a job in the short term and still claim the SEISS grant. Oh, and there's no VAT on Kindle books any more 📘 Bounce Back Loan Scheme (BBLS) You'll remember (pop quiz!) that in our update last week we reflected on how only 16,000 loans had been approved under the Business Interruption Loan Scheme. That's a fairly low number when you consider there are c. 5M businesses in the UK. I wish I could say it's because only a handful needed support, but in reality - and having seen some bank application forms - the information required is just waaaaay too much for most sole traders, who don't produce formal management accounts or cash flow forecasts, for example. So, the new BBLS is aimed at the smallest businesses, with turnover measured in the tens of thousands rather than millions. In summary, this is; - a 'micro-loan' of between £2,000 and £50,000 (max 25% of turnover) - interest rate set at 2.5% - no repayments for the first 12 months - loan terms up to 6 years - 100% backed by the govt, so there is no risk to the bank - once approved, cash expected within 2 working days - self-certified online application This last point is crucial - banks won't need reams of reports, or for you to send in copies of accounts etc. You will just need to certify your ability to repay the loan. Remember, the loan is still debt, but at these very relatively favourable rates I can see a lot of businesses taking this opportunity to 'refinance' other debt they may have, especially overdrafts, where the rate is significantly higher than 2.5%. When and How do I get this? You can apply through any bank who is an accredited lender - all the usual suspects, there are 52 in total - AND who choose to offer the scheme (it's not mandatory). I'd recommend starting with your existing bank to speed things up. The government tell us the scheme will start on Monday 4th May. In my opinion, I cannot see this being enough time for the bank to update all their systems, but we shall see. That's all the information we have right now. Give me a call if you think you might want to apply for the loan and we'll let you have more information as we get it. Self-Employed Income Support - Your Questions This week has seen a lot of you asking for clarification on a few points of this scheme, and whether you could inadvertently be disqualified. It doesn't help that HMRC's guidance is sometimes contradictory, and changes from day to day. I'm pleased to say that I have now had sight of the Direction from the Treasury, which was only signed on Thursday. This has the force of law and therefore trumps any 'guidance' you may read. If you're bored, here's a link. What If I Get A Job? Don't worry. The govt accepts that the self-employed are a resourceful bunch, and you might have taken on employment recently whilst your business is shut. That's OK; provided this is short term, you'll still meet the criteria which includes: - you have been trading in 2018/19 and 2019/20 - you intend to continue trading at some point in the year ending 5th April 2021. There is no requirement for you to be trading right now. This is entirely logical as many businesses have been forced by the govt to shut and cannot trade. The only potential issue I can see with the above criteria is if your short-term job becomes permanent and you don't return to self-employment, you could be asked to repay the grant. Even then, however, note the word "intend"; provided you can show your intention was to return to your business after CV19, it would seem that you would qualify regardless of what actually happens. What ARE My Trading Profits? Another great question. 'Profit before tax', 'Net profit', 'Taxable Profit' and so on. Accountants like to have lots of different ways of measuring profit, which muddies the water a little bit. 🤷♂️ Mr Sunak has confirmed that it will be based on "Step One of Section 23 of the Income Tax Act 2007". Before you dust off your tax legislation, let's save you the hassle: it's the profits on which your tax charge is calculated, before deducting any losses brought forward from previous years. If you look at your SA302 "Tax Year Overview", it's the value at the top. If you're unsure please give me a call. If we don't already prepare your tax return, you'll need to send me the last three years' figures and I'll take a look for you. But I'm in a Partnership? Simples; it's your share of the profits, as shown on your tax return. It doesn't matter how much the partnership made overall. Can I Amend My 2018/19 Tax Return? Yes, and No. You can amend your tax return if there was an error in it, for example. However, the govt has made it clear in their Direction that returns amended from 26th March [when the SEISS was announced] will be ignored for the purposes of the scheme. This seems reasonable, as the risk of fraud at a national level would be too high. Sadly this will mean some people with genuine amendments to make may be disadvantaged. Ok, enough about that...what else might have slipped your notice? VAT on PPE and e-books I'll confess something here. I'm not ashamed to say that I had assumed - as you might - that all PPE was VAT-free. Indeed, safety boots, hard hats, car seats and the like ARE zero-rated. But disposable gloves, gowns and masks are charged to 20% VAT. The NHS and care homes usually cannot reclaim VAT on PPE, so this is a real cost to them. And as VAT is 20% on the purchase price - which itself has been shooting up recently as demand outstrips supply - this is a chunky cost. The govt have announced that supply of these items will be zero-rated from 1st May to 31 July 2020. This is only temporary, which is disappointing. However... Whatever your thoughts on the EU, they still hold the cards in respect of VAT rate changes. They recently agreed to a series of EU-wide temporary VAT reliefs, and the UK is taking advantage of these. Once CV19 passes, it will be up to the EU [in the transition period] to allow the reliefs to stay in place. Hot on the heels of PPE - and more relevant to mental health than physical health - is the zero-rating of VAT for e-publications, including kindle books and the like. Paper books have always been VAT-free but the "reading tax" still applied to books in digital form. On a personal note, as someone with an interest in supporting the blind [through www.moorvision.org], it's sad to see this change does NOT apply to audiobooks. These are a lifeline for the visually impaired, and it's something we are asking the govt to review. In reality, we don't expect any changes until the transition period is over. From 1st May, there will be no VAT on digital books, magazines and so on. Whether this results in a 20% cut to prices - or if Amazon just pocket the difference - remains to be seen. This cut, however, remains permanent; the EU has allowed member states to bring VAT on ebooks into line with on physical books. Let's just hope PPE follows suit. Supporting Each Other If your business has been hammered by CV19 but is still able to continue trading in some capacity, can we use the power of everyone in this group, and their contacts, to generate some work for you? Regardless of whether you're a client or not - it really doesn't matter - tell us about your business, how it's been affected, how we can help and what services you are still able to offer under lockdown. Perhaps, someone might just be after that right now... 🤞 |